The Missing Variable in Underwriting Wildfire Risk

Why the next generation of wildfire models will be built on parcel-level and community mitigation intelligence

Welcome to Ground Truth, OmniGeo’s publication on the intersection of geospatial AI and physical risk — for the people building in Earth observation and the underwriters, asset owners, and risk teams who have to trust them.

In late 2025, Headwaters Economics, the wildfire analytics firm Pyrologix, and the U.S. Fire Administration published a two-part study with a deliberately boring title: Wildfire Risk Indices and the Built Environment. Part one is an inventory: the authors started with more than 150 wildfire risk models, narrowed down to 59 that met their criteria, and scored each on how well it captured the built environment and whether it could run at national scale. Part two is the interesting part: they interviewed 30 subject matter experts, including fire physicists, structural engineers, catastrophe modelers, and insurers who do this work, and asked them how models are broken today.

Buried in the findings is the reason we started OmniGeo.

This field of experts largely agrees that one of the most important datasets needed to reduce wildfire losses does not yet exist. That matters because wildfire is no longer just a forestry problem. It’s an insurance problem, a mortgage problem, a municipal finance problem, and increasingly, a household balance sheet problem.

The question isn’t whether a wildfire will burn in a particular area. We have a good understanding of this. Any area that abuts a moderate or higher wildfire risk area has the potential to burn, especially in areas with high wind potential. The question now is which homes burn, which survive, and whether we can predict the difference before the fire arrives. This study is remarkably transparent in asserting that our wildfire models still struggle to do that.

The Wildfire Modeling Paradox

Over the last two decades, wildfire modeling has become very sophisticated. We can model fuel loads, topography, wind fields, drought stress, ember transport, and fire spread across landscapes at scales that would have seemed impossible a generation ago. Yet some of the most destructive fires in recent history have exposed a persistent blind spot: the built environment.

As Headwaters Economics notes, most existing wildfire models remain fundamentally optimized for understanding how fire moves through vegetation, not how it propagates through neighborhoods. Structure-to-structure ignition, building materials, parcel conditions, and mitigation actions remain poorly represented in most operational risk models. That distinction may sound academic, but it isn’t.

When a fire enters a neighborhood, the rules change. A burning cedar fence behaves differently from a ponderosa pine. A wood shake roof behaves differently from concrete tile. A home with five feet of defensible space behaves differently from one with vegetation touching the structure.

These differences often determine single losses measured in hundreds of thousands or millions of dollars. Yet they remain surprisingly difficult to measure consistently across entire states.

What the Experts Said

The second phase of the Headwaters study interviewed 30 wildfire risk experts across disciplines. The findings were fascinating. There was disagreement about many things: whether behavioral change or better models matter more, whether physics-based models or simplified operational models are the future, and how close we are to accurately modeling structure-to-structure fire spread. But there was striking agreement around one issue: a lack of data.

As one interviewee put it: “Models are only as good as the data inputs.” That sounds obvious, yet the implications are enormous. Among the report’s most important recommendations was the need for better datasets that capture:

Building-level characteristics

Parcel-level conditions

Ember transport dynamics

The impact of mitigation activities on fire behavior

The report explicitly identifies remote sensing as one of the most promising paths for developing these datasets at scale. One of the most comprehensive recent reviews of wildfire risk modeling concluded that one of the highest-leverage opportunities isn’t another fire model, but rather better measurement.

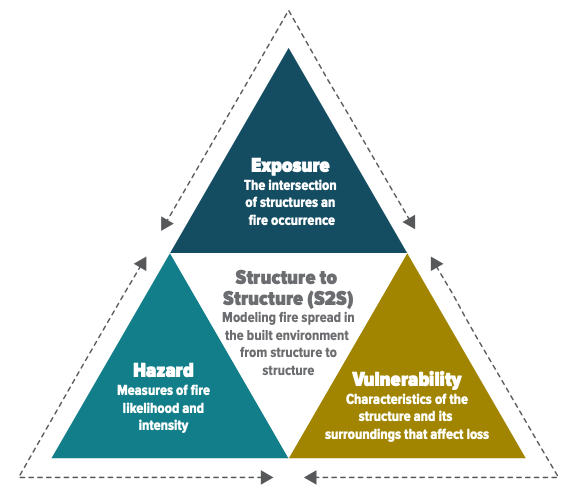

Hazard Is Not the Same as Vulnerability

This distinction gets lost surprisingly often. Wildfire risk is typically described as a combination of hazard, exposure, and vulnerability. Combine the three, and you can measure the risk and size of loss.

Hazard is where most attention goes. How likely is a fire? How intense could it become? How fast might it spread? These questions are critically important, but they don’t explain why one home survives while another burns. That is defined by vulnerability.

Vulnerability is measured at the parcel level. What is the roof made of? How much vegetation exists within five feet of the structure? Has mitigation occurred? Has the roof deteriorated? Did the homeowner replace wood fencing with non-combustible materials? Did defensible space improve since the last inspection? These are fundamentally measurement questions, not modeling questions.

However, the challenge is that they have historically been expensive, manual, and difficult to update.

The Cost of Not Knowing

The repercussions of this can be seen across the risk value chain. Insurance carriers raise premiums. Others stop writing policies entirely. Homeowners invest thousands of dollars in mitigation without knowing whether it materially changes risk or the cost of their insurance policy. Communities struggle to prioritize interventions and invest in neighborhood-level mitigation. Regulators push for more granular understanding while insurers often rely on incomplete information.

The result is a market operating with partial visibility. And partial visibility is expensive. One of the most interesting observations from the Headwaters report is that current wildfire models often face a tradeoff. Models that scale nationally often lack the precision of the built environment. Models with detailed precision often struggle to scale nationally.

Solving this bottleneck requires capturing that precision at a national scale. The problem is not a lack of imagery, compute, or machine learning. It is a lack of scalable, validated measurements of the physical conditions that actually influence loss.

A Remote Sensing Opportunity

The report repeatedly points toward advances in remote sensing, machine learning, and improved data collection as key enablers of the next generation of wildfire risk models. That observation mirrors something we’ve seen repeatedly across insurance, infrastructure, utilities, and climate risk.

The world has become incredibly good at collecting images. We’re still surprisingly bad at extracting physical intelligence from them. The challenge is no longer obtaining pictures of a property, but rather understanding what those pixels reveal about materials, condition, vegetation, and vulnerability. The opportunity is to convert imagery into measurement using novel methods. And that’s what we’re doing at OmniGeo.

The Measurement Decade

The first generation of wildfire risk models focused on understanding fire. The next generation will need to understand properties: not just where they are, but what they’re made of, how they’re changing, and whether mitigation actually works.

The Headwaters report does not prescribe a specific technical solution, but it does clearly identify where our knowledge breaks down. The industry needs better data on buildings and parcels, better visibility into mitigation, and scalable ways to collect that information.

That may turn out to be one of the most important opportunities in wildfire risk over the next decade. Because before we can accurately model vulnerability, we first have to measure it.

And right now, that’s still the hardest part.

The measurement layer behind Ground Truth

OmniGeo’s first product, OmniFire, closes the earth measurement gap for insurers in wildfire-prone areas. OmniFire turns standard imagery into parcel-level measurements of what a property is actually made of, including roof material, defensible space, and fuel moisture. It’s vulnerability measured at scale and it’s live today. If you underwrite, price, or manage wildfire risk, visit www.omnigeo.ai/omnifire to learn more.